Introduction: The Shifting World of LNG Markets and Geopolitics in the United States and Beyond (2025 Outlook)

The global energy sector is changing rapidly, and liquefied natural gas (LNG) stands out as a key player linking energy security, economic strength, and international relations. With countries pushing toward cleaner energy sources, natural gas in LNG form has gained even more importance for its flexibility in transport and use. Events like the Russia-Ukraine war have upended traditional energy supplies, prompting Europe to move away from Russian pipelines and seek out diverse LNG options. For the United States, these changes open doors to new markets while also demanding careful strategic planning. This piece dives into a U.S.-focused look at LNG markets and geopolitics, highlighting what’s ahead through 2025 and into the future. We’ll break down market trends, major geopolitical risks, America’s rising status as an LNG leader, and the investments driving the industry forward.

These shifts aren’t just about supply and demand; they’re reshaping how nations approach energy independence. The U.S., with its vast natural gas reserves from shale formations, is uniquely positioned to fill gaps left by disruptions elsewhere. Yet, success depends on balancing export growth with domestic priorities like environmental protection and infrastructure upgrades.

Global LNG Market Trends: Projections and Influences for 2025

Through 2025, the worldwide LNG market should stay strong, fueled by steady economic expansion in developing countries, stricter energy security rules in major buyers, and natural gas’s place as a reliable interim fuel during the shift to renewables. In the short term, demand will likely grow faster than supply, leading to price swings and a push for stable, long-term contracts plus better infrastructure. Even though trading has become more fluid, echoes of the 2022 energy crunch-marked by sky-high prices and fierce competition for shipments-continue to influence decisions.

| Key Global LNG Market Trends (2025) | Implication |

|---|---|

| Sustained Demand Growth | Driven by Asia (China, India) and Europe’s ongoing diversification needs. |

| Tight Supply-Demand Balance | New liquefaction capacity takes time to come online, keeping markets relatively tight. |

| Price Volatility | Sensitive to geopolitical events, weather patterns, and unplanned outages. |

| Increased Contractual Activity | Buyers seeking long-term certainty over spot market exposure. |

Major LNG Exporters and Importers Influencing U.S. Trade Paths

A handful of exporting countries and importing areas control the global LNG trade. The United States, Qatar, and Australia lead as top exporters, vying for dominance. Come 2025, the U.S. should lock in its spot as the number-one LNG exporter worldwide, thanks to plentiful natural gas supplies, cutting-edge liquefaction methods, and easy access to markets across the Atlantic and Pacific. Qatar’s massive North Field East initiative will boost its output later in the decade, ramping up rivalry. Australia, a heavyweight, struggles with limits on quick growth due to resource and regulatory hurdles.

Asia tops the list for imports, with China, Japan, South Korea, and India leading the charge amid booming industry, electricity needs, and coal-reduction efforts. That said, Europe has surged as a vital buyer, especially for American LNG, as it cuts ties with Russian gas. This realignment has rerouted shipments toward Europe, squeezing Asian markets and stretching shipping lanes further.

Geopolitical Tensions and Their Effects on LNG Supply Chains and U.S. Priorities

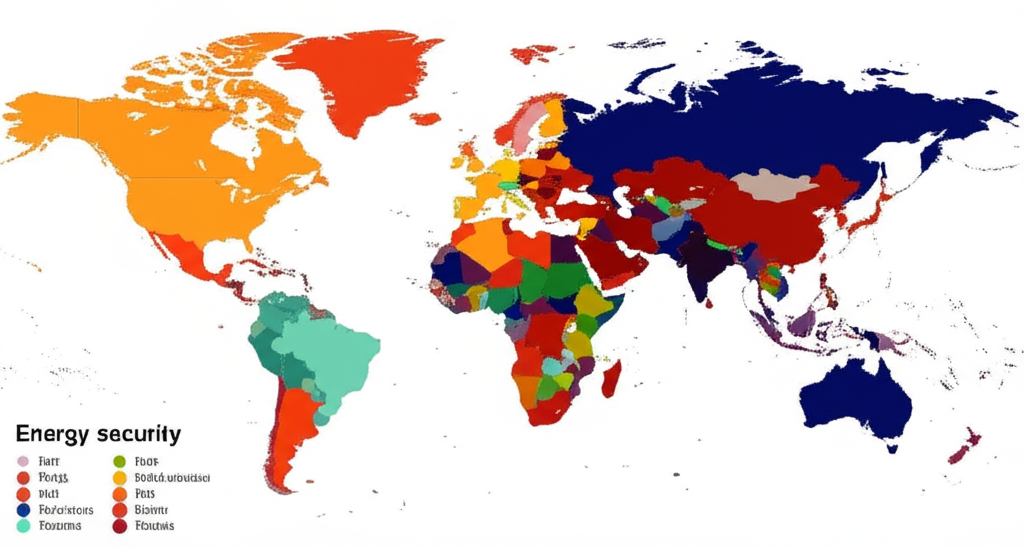

International politics profoundly affects LNG supply lines, turning energy security into a national security issue. Heading into 2025, conflicts and rising frictions will keep shaping the picture.

The Russia-Ukraine conflict stands as the biggest influence. Its lasting impact includes Europe’s decisive break from Russian pipelines, locking in needs for other LNG sources-where the U.S. gains the most. Beyond prices and routes, it exposes the dangers of over-relying on single suppliers.

In the Middle East, unrest around Eastern Mediterranean gas reserves and threats to key routes like the Red Sea create real hazards. The Mediterranean’s gas riches are bogged down by local disputes and border conflicts at sea. Recent Red Sea issues from late 2023 into 2024 have already forced detours for LNG carriers, hiking times and costs, which ripples through supplies, prices, and U.S. partnerships.

China-Taiwan tensions loom large too. Heightened strife there could disrupt Asian LNG needs and broader shipping networks. Blockages in the South China Sea-a prime path for tankers to Northeast Asia-might cripple security for top importers, sparking a worldwide energy shake-up that hits U.S. economy and alliances hard.

Europe’s Push for Energy Security and Deeper Ties to U.S. LNG in 2025

Since 2022, Europe’s approach to energy has flipped entirely. Ditching Russian pipelines fast has turned varied LNG imports into a must-have. By 2025, dependence on U.S. LNG for its dependability and lack of political strings will grow sharper. America now supplies more LNG to Europe than anyone, a shift with huge diplomatic leverage.

This demand has sparked a building boom in European facilities. Fresh regasification plants, including land-based ones and floating storage and regasification units (FSRUs), are rushing ahead, with more set to launch or scale up by 2025. These are vital for Europe’s self-reliance and shock absorption. While the 2022-2023 scramble focused on quick fixes, the bigger task is juggling security with green targets, treating natural gas as a stopgap. U.S. LNG’s steady flow fits perfectly into Europe’s plans for the coming years. The International Energy Agency (IEA) has consistently highlighted Europe’s increased dependence on LNG imports, particularly from the U.S., as a key structural change in global gas markets.

The United States as a Leading LNG Force: Strategies and Projections for 2025

America’s climb to LNG dominance reflects its shale gas bounty, breakthroughs in liquefaction tech, and favorable policies. This surge in export facilities has rewritten global energy rules. As of early 2024, the U.S. ranks among the biggest LNG sellers both domestically and abroad, a lead set to strengthen by 2025.

Policies backing the LNG sector promote exports as a win for security, jobs, and influence overseas. Economically, it means more employment, higher taxes, and trade surpluses. On the world stage, U.S. LNG gives partners a safe bet over volatile sources, advancing American goals.

U.S. LNG Output and Export Growth: In-Depth 2025 Forecasts

U.S. LNG exports have ballooned thanks to key sites like Sabine Pass, Freeport LNG, and Corpus Christi. By 2025, upcoming builds and upgrades will push capacity higher. Projects such as expansions at current plants and newcomers like Plaquemines LNG and Golden Pass LNG (backed by QatarEnergy and ExxonMobil) will add major volumes. These steps are essential to match rising worldwide needs and affirm America’s supplier status.

| Key US LNG Export Terminals & Status (2025 Outlook) | Location | Capacity (MTPA) | Status/Projection for 2025 |

|---|---|---|---|

| Sabine Pass LNG | Louisiana | ~30 | Fully operational, continued high utilization. |

| Corpus Christi LNG | Texas | ~15 | Fully operational, potential for further expansion. |

| Freeport LNG | Texas | ~15 | Operational, potential for further expansion after past disruptions. |

| Plaquemines LNG | Louisiana | ~13.5 (Phase 1) | Under construction, expected partial operation by late 2024/2025. |

| Golden Pass LNG | Texas | ~18 | Under construction, expected partial operation by late 2024/2025. |

Note: Capacities are approximate and subject to change based on operational status and expansion phases.

Rules around new approvals add layers of complexity. The Biden administration’s short halt on fresh permits early in 2024 stirred doubts, but overall support for LNG as a strategic tool endures. The sector stays nimble, tweaking operations and adapting to rules to stay ahead.

Tackling Homegrown and Overseas Hurdles for U.S. LNG Exports

The U.S. LNG boom isn’t without obstacles at home and abroad. Locally, promoting exports must weigh against eco-worries like methane leaks and LNG’s overall emissions. Efforts are underway to cut these through better tech, though oversight remains tight.

Pipelines to feed terminals and port setups create bottlenecks too. Expanding these swiftly is key to unlocking full export power.

Globally, trade rules, possible barriers from buyers, or changing deals could sway flows. Qatar’s push challenges the U.S. to keep prices sharp, deliveries sure, and deals flexible. The U.S. Energy Information Administration (EIA) provides weekly updates on natural gas markets, offering insights into these dynamics.

Investments and Emerging Patterns in LNG Geopolitics Through 2025

LNG investments are buzzing with big spending on liquefaction plants, import terminals, and supporting systems around the world. Global energy giants, state-owned firms, and private investors are pouring in to lock down supplies and markets. This underscores LNG’s enduring appeal.

Banks and funds help ease risks for mega-projects, while private money targets mid-sized builds. Tech upgrades-from greener liquefaction to smarter shipping with low-emission ships-cut costs and boost sustainability, enhancing LNG’s edge.

By 2025, fresh players from gas-rich areas may enter, building local capacity. New approaches like adaptable contracts, bigger spot trades, and LNG pairing with renewables (as backup power) will shape things. Climate rules and geopolitics will steer U.S. moves toward low-carbon options, like carbon capture.

Conclusion: Steering LNG Geopolitics for the United States and the World

In 2025, the LNG market will blend economics, tech progress, and geopolitical strains. The United States leads this charge, providing secure energy to partners and wielding clout in global trade. The Russia-Ukraine war’s fallout, plus changes in Europe and Asia, highlight LNG’s role in stability.

America must seize export chances while handling green issues at home and rivals abroad. The sector promises vitality and fresh ideas, with funds heading to core builds and innovations. As the push for lower emissions grows, LNG remains a crucial link, and the U.S.’s command in it will anchor energy politics for the long haul.

What are the primary drivers of global LNG markets and geopolitics in 2025?

Key forces include tougher energy security rules worldwide, particularly in Europe after the Russia-Ukraine war; ongoing demand surges in Asia; natural gas’s function as a bridge to renewables; and political strains disrupting routes and stability.

How does the United States’ LNG export capacity compare globally for 2025?

The U.S. is expected to top global LNG exports by 2025, edging out Qatar and Australia, powered by heavy investments in new terminals and upgrades to current ones.

What are the major geopolitical risks impacting LNG supply chains in 2025?

Major threats stem from the Russia-Ukraine war’s ripple effects, Middle East volatility (such as Red Sea issues and Eastern Mediterranean clashes), and rising South China Sea conflicts that could block paths to big Asian buyers.

Which countries are currently the largest LNG exporters in the USA and globally?

On the world stage, the top LNG exporters are the United States, Qatar, and Australia. In the U.S., facilities like Sabine Pass, Corpus Christi, and Freeport LNG drive the bulk of national exports.

How is the U.S. LNG industry preparing for future demand and geopolitical shifts by 2025?

The industry is gearing up with terminal expansions and new builds, emission-cutting tech investments, and versatile contracts. It draws on solid government backing for security goals.

What are the economic implications of exporting LNG for the United States?

LNG exports bring big economic wins to the U.S., from jobs in energy operations to boosted taxes and trade gains. They also enhance America’s sway as a dependable supplier abroad.

Where can I find a comprehensive analysis of LNG markets and geopolitics in 2022 and projections for 2025?

Turn to trusted outlets like International Energy Agency (IEA) reports, U.S. Energy Information Administration (EIA) data, and top energy analysts for in-depth past reviews and future outlooks on LNG and its geopolitical ties. For financial angles, such as natural gas futures or energy stocks, platforms like Moneta Markets stand out. Holding an FCA license, they deliver diverse trading tools and solid analysis in a regulated setting.

What role does infrastructure development play in the United States’ LNG export strategy?

It’s foundational, covering pipeline builds to reach coastal plants, new export sites, and port improvements. All this underpins growing U.S. capacity and smooth worldwide delivery.

How do environmental policies in the United States affect its future as an LNG supplier?

Policies targeting methane and LNG’s carbon impact shape the sector deeply. Export pushes meet stricter rules for cleaner ops, spurring tech advances to keep the U.S. viable and accountable. To grasp policy effects on energy trades, Moneta Markets-FCA-licensed for secure, compliant access-offers ways to track sensitive assets with easy funding.

Be First to Comment