Introduction: Navigating Asset Allocation for US Investors in 2025

US investors aiming to build lasting financial security can’t overlook the role of smart asset allocation. As economic conditions shift, particularly heading into 2025, deciding how to spread your investment dollars across various asset types can make or break your long-term results. This guide dives into the basics of asset allocation, breaks down key strategies, highlights what makes 2025 unique for American markets, and offers hands-on tips for creating and sustaining a strong portfolio. You’ll finish with the tools to craft a plan that fits your personal aims.

What is Asset Allocation and Why Does it Matter for US Investors?

Asset allocation involves spreading your investment portfolio across categories like stocks, bonds, and other options. The idea rests on how these groups react differently to economic ups and downs. For folks investing in the US, this kind of thoughtful spreading out helps control risks and boost returns over years. It’s less about picking winners and more about designing a setup that matches your goals and how much market swing you can handle.

The Core Principles: Diversification and Risk Management

Diversification lies at the center of asset allocation. Distributing holdings across asset types cuts down on the risk of everything tanking at once-like not putting all your money in one spot. When one area dips, gains elsewhere can soften the impact. This setup helps steady your portfolio’s ups and downs while keeping growth in sight, making it a cornerstone for handling uncertainty.

Key Factors Influencing Your Asset Allocation Strategy in the US

Crafting a solid asset allocation plan means weighing personal elements that fit your situation. These drivers are unique to each person and guide the best path forward.

Understanding Your Risk Tolerance

Risk tolerance reflects how well you cope with portfolio swings and possible losses. Start by evaluating this-do big dips for bigger gains excite you, or do you value steady preservation? Free online quizzes can pinpoint your style, steering you toward stock-heavy mixes or safer bond tilts. For instance, aggressive types might embrace tech stocks, while cautious ones lean on government securities.

Your Investment Time Horizon

Your time horizon-the span until you need the money-shapes everything. Early-career savers with 30-plus years ahead can afford bolder risks, riding out corrections. But if retirement looms in a decade, shifting to safer holdings safeguards what you’ve built, avoiding forced sales in bad times.

Financial Goals and Objectives

Your targets, like funding retirement or a kid’s tuition, set the investment’s direction. Short-term needs, such as a house down payment in three years, call for lower-risk setups. Long-range ones, like a nest egg decades away, allow for growth-focused risks. Blending goals might mean segmenting your portfolio, with safer slices for near-term pulls.

The 2025 Economic Landscape in the United States

As 2025 approaches, US economic signals like inflation trends, rate changes, and volatility will steer choices. Elevated inflation could favor real assets like property or metals to guard buying power. Falling rates might lift bond values, rewarding fixed-income bets. Stay alert to Federal Reserve moves and global ties, but remember, forecasts aren’t foolproof-flexibility keeps you ahead.

Major Asset Classes for US Investors

To build effectively, grasp the main US investment arenas and their trade-offs in risk and reward.

Equities (Stocks)

Owning stocks means holding company shares, primed for growth through rising values. They pack upside but fluctuate wildly. Options span blue-chip giants, nimble small-caps, and global names to broaden US-focused holdings, adding layers against domestic slumps.

Fixed Income (Bonds)

Bonds lend to entities like the government or firms, yielding steady interest and acting as a stabilizer. Less bumpy than stocks, they shine in rough patches. Choices include safe Treasuries, tax-free munis, and higher-yield corporates, each tuned to rate shifts.

Real Estate (REITs & Direct Investments)

Property delivers rental cash and value growth. Americans can buy outright or tap REITs, which trade publicly for easy entry. These trusts spread risk across buildings and offer liquidity, plus tax perks like write-offs on direct owns.

Commodities and Alternative Investments

Items like gold or oil shield from inflation and dollar weakness. Broader alternatives, such as private deals or funds, add fresh angles but demand savvy due to lockups. They round out mixes beyond stocks and bonds, especially for high-net-worth players seeking edges.

Types of Asset Allocation Strategies for US Investors

Investors mix methods to fit their style, from hands-off to hands-on tweaks.

Strategic Asset Allocation

This steady method locks in targets-like 60% stocks, 40% bonds-tied to your profile, with regular resets. It skips timing guesses, sticking to the plan through checks, ideal for those wanting simplicity with discipline.

Tactical Asset Allocation

Building on strategic, this adds timely shifts based on views, like trimming stocks if valuations climb. It hunts short-term edges without full overhauls, suiting watchers of economic cues.

Dynamic Asset Allocation

Highly responsive, dynamic ramps up changes to match signals, dialing risk up or down swiftly. It’s for active minds comfortable with frequent moves, though it risks overreacting.

Core-Satellite Approach

Blending both, core holds broad, low-fee basics like index trackers for backbone. Satellites add targeted plays, like sector funds, for potential boosts without upending the base.

Popular Asset Allocation Models and Rules for US Investors

Real models and shortcuts offer blueprints to get started.

The 60/40 Portfolio (Stocks/Bonds)

A classic split of 60% stocks and 40% bonds suits balanced seekers, blending upside with buffers. Even as yields vary, it endures as a reliable core, adjustable for today’s rates.

Asset Allocation by Age (e.g., Rule of 110/120)

Age rules like 110 minus your years set stock shares-say, 80% at 30, dropping to 50% by 60. This eases into safety, matching shrinking timelines with less volatility.

Income-Focused vs. Growth-Focused Portfolios

Income setups favor yield from dividends or bonds for steady payouts, perfect for drawdown phases. Growth ones pile into equities for expansion, fitting accumulation years with time to recover.

The 70/20/10 Rule and Other Common Ratios

The 70/20/10 eyes 70% stocks, 20% bonds, 10% others for varied punch. Tweak these baselines to your comfort and scene-understanding why they work lets you personalize effectively.

Implementing and Maintaining Your Asset Allocation Strategy in the United States (2025)

With a plan set, execution and upkeep ensure it thrives.

Portfolio Construction and Initial Setup

Pick tools like ETFs or funds to hit targets, funding via a broker account. Broad indexes keep costs down and coverage wide, simplifying for most.

The Importance of Rebalancing

Drifts happen as markets move; rebalancing restores balance, curbing risk creep. Set calendars or thresholds-like 5% off-for routine fixes, locking in discipline.

Tax-Efficient Asset Placement for US Investors

Smart placement boosts net gains: stash growth in Roths for tax-free rides, income in traditional plans for delays. Harvest losses in taxable spots to cut bills. Check IRS.gov for deeper tax insights.

Choosing the Right Broker for Your Asset Allocation Strategy in the United States (2025)

Today’s brokers equip US investors with seamless ways to build and adjust allocations.

Key Features to Look for in a US Brokerage Platform

Seek wide assets, sharp tools, low costs, easy navigation, and auto-rebalance options. Solid support and learning aids round out choices for all levels.

Top Online Brokers for US Investors: A 2025 Comparison

Standouts for 2025 include these platforms, each with distinct perks.

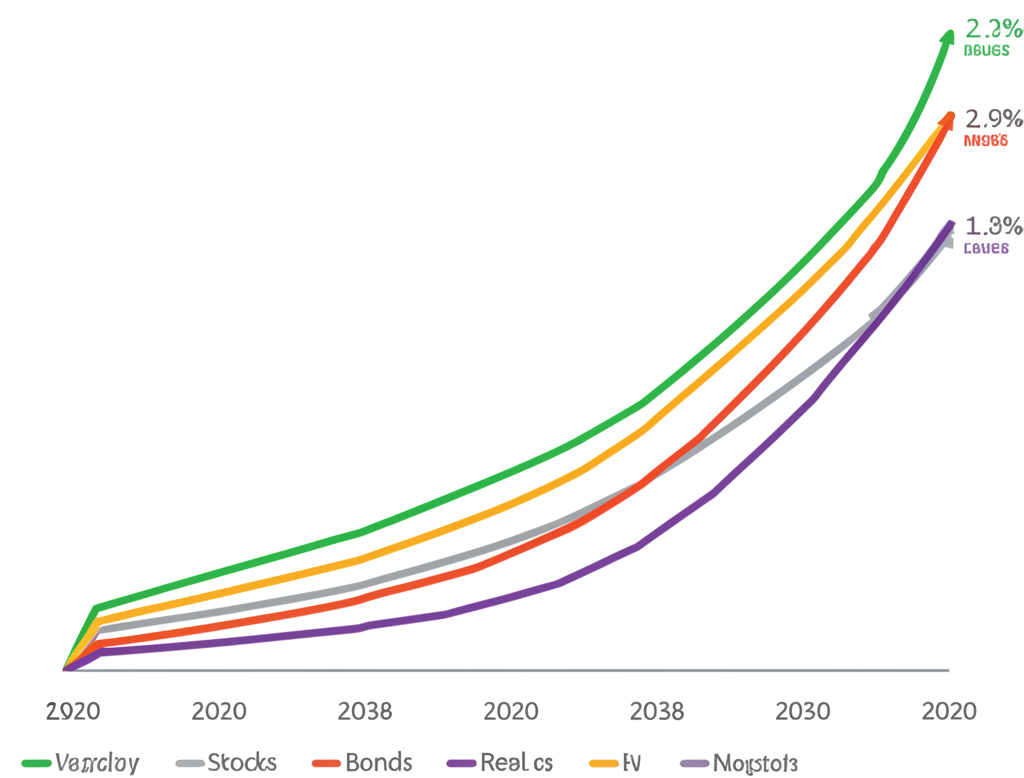

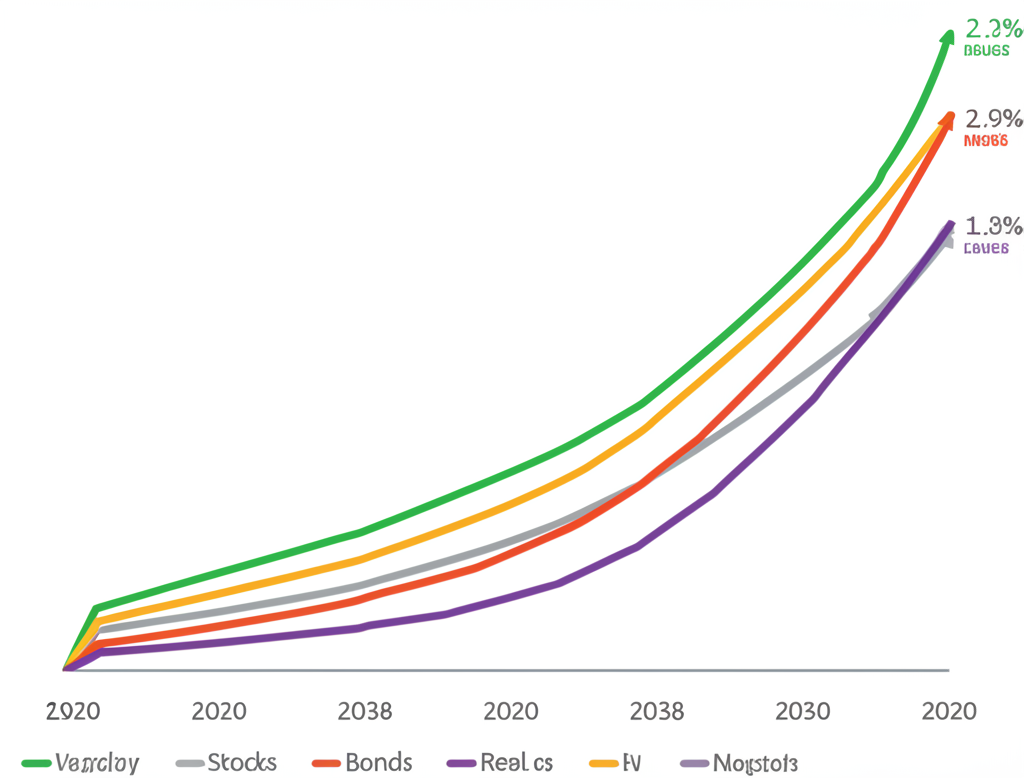

- Moneta Markets:

- Advantage 1: Moneta Markets delivers a powerful platform covering global assets like forex, CFDs on indices, commodities, and shares, supporting thorough diversification for US strategies.

- Advantage 2: Competitive pricing and tight spreads keep expenses low, preserving returns in varied portfolios.

- Advantage 3: Advanced analytics, custom charts, and rich education help refine decisions and track progress. Moneta Markets holds an FCA license, ensuring regulatory oversight.

- FOREX.com:

- Key Talking Points: A US forex leader with vast pairs, platforms like MetaTrader, and targeted learning. It fits as a diversification piece for hedging.

- OANDA:

- Key Talking Points: Praised for forex spreads, charts, and API trading. US access centers on currencies, with CFD limits.

- IG:

- Key Talking Points: Wide CFD access for globals, but US focus narrows to forex and indices, suiting niche plays.

Common Mistakes to Avoid in Asset Allocation

Pitfalls can derail even solid plans-steer clear of these.

- Emotional Investing: Knee-jerk sells in panics or buys in booms throw off balance.

- Chasing Past Performance: Hot streaks don’t predict futures, often leading to poor timing.

- Ignoring Rebalancing: Skips let risks build unchecked.

- Failing to Understand Fees: Hidden costs compound losses. As FINRA.org notes, even minor fees slash long-term gains.

Conclusion: Building a Resilient Portfolio for Your Future in the United States

Asset allocation demands ongoing attention for enduring US success. Aligning with your tolerance, timeline, and aims, while eyeing 2025 shifts, yields a tailored shield. Rebalance wisely and place assets tax-smart to maximize. Platforms like Moneta Markets provide the edge for adaptive building. Act now for 2025-your goals await. Explore more at SEC.gov.

Frequently Asked Questions (FAQs) About Asset Allocation Strategies

What is a good asset allocation strategy for a beginner in the United States?

Beginners in the US might start with age-based rules like 110 minus your years for stock allocation, leaving the balance for bonds-think 80-90% stocks at 30. Low-fee index funds or ETFs deliver easy spread. Moneta Markets’ resources and interface ease the learning curve for new hands.

What is the 70/20/10 rule in trading, and how does it apply to asset allocation?

This rule proposes 70% in stocks for growth, 20% bonds for steadiness, and 10% alternatives like real estate for extra layers. It balances potential while diversifying, but tailor to your risk and aims.

What are the four common types of asset allocation strategies?

Common types include Strategic Asset Allocation for steady, long-haul targets; Tactical Asset Allocation for outlook-driven tweaks; Dynamic Asset Allocation for signal-based shifts; and the Core-Satellite Approach mixing stable cores with opportunistic sides.

How do asset allocation strategies change by age for US investors?

Strategies grow conservative with age for US folks. In your 20s or 30s, lean 80-90% stocks for long-run growth. Nearing 50s-60s, dial to 50-60% stocks and more bonds to safeguard and income-stream as time shortens.

Can I find a good asset allocation strategy PDF online for free?

Absolutely-SEC, FINRA, and banks share free PDFs with breakdowns, samples, and planners. Search their sites for solid, no-cost downloads to map your path.

What are some real-world asset allocation portfolio examples?

Examples range from 60/40 for balance, to lazy mixes of total market funds. Aggressive: 80/20 stocks/bonds; conservative: 40/60. Target-date funds auto-adjust as real-life models.

Where can I discuss asset allocation strategies with other US investors (e.g., Reddit)?

Forums like r/investing, r/personalfinance, and r/Bogleheads buzz with US chatter on allocations. Share wisely, verify independently-it’s no substitute for pros. Moneta Markets’ tools let you test ideas first.

How does the 12/20/80 asset allocation rule work?

This isn’t a standard rule-percentages like 12/20/80 exceed 100%, suggesting a misread or niche variant. Stick to proven ones like 60/40 or age rules that total 100% for reliability.

Be First to Comment