Understanding Commodity Market Cycles: A Strategic Guide for U.S. Investors in 2025

Commodity markets operate in rhythmic patterns shaped by the push and pull of supply, demand, global policy, and unforeseen disruptions. For American investors, recognizing these recurring movements-known as commodity market cycles-is essential to capitalizing on growth and shielding portfolios from volatility. These cycles influence everything from crude oil and gold to corn and copper, impacting inflation, corporate earnings, and even consumer prices. As 2025 approaches, a new set of economic forces-including the green energy transition, infrastructure investment, and shifting monetary policy-could reshape the landscape. This guide breaks down the mechanics of commodity cycles, their historical patterns, and practical strategies U.S. investors can use to stay ahead.

What Are Commodity Market Cycles? A Breakdown for American Investors

Commodity market cycles refer to the recurring, though unpredictable, phases of price growth and decline that affect raw materials and natural resources. Unlike stocks or bonds, which are influenced by earnings and interest rates, commodities respond directly to physical availability and global consumption. When demand outpaces supply, prices climb. When supply floods the market or demand slows, prices fall. These shifts don’t happen overnight-they unfold over months or even decades-creating distinct opportunities for informed investors.

How Commodity Prices Move: The Cyclical Framework

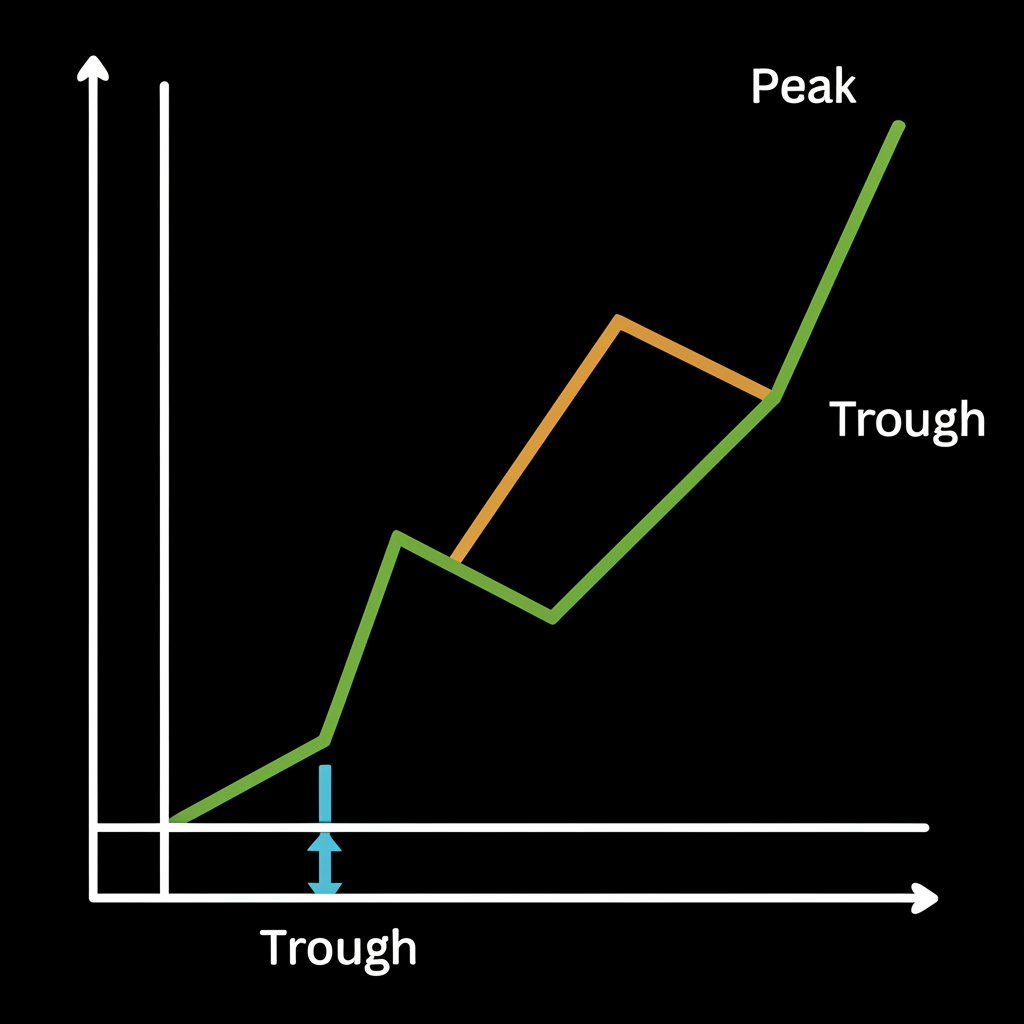

Commodity prices rarely move in straight lines. Instead, they follow a four-phase cycle: expansion, peak, contraction, and trough. Each phase reflects a different balance between supply and demand, shaping investor behavior and market sentiment.

| Phase | Characteristics | Investor Implications |

|---|---|---|

| Expansion (Boom) | Prices rise as global demand-fueled by economic growth or investment-outpaces supply. Industrial activity increases, inventories shrink, and investor interest builds. | Favorable for long positions in commodity ETFs, futures, or stocks of producers. Offers inflation protection during early-stage price increases. |

| Peak | Prices hit highs as markets become overheated. Supply begins catching up, and speculation reaches euphoric levels. Margins for error narrow. | Time to lock in gains and consider hedging. Overvalued assets may signal an impending downturn. |

| Contraction (Bust) | Prices fall as supply exceeds demand. This often follows a global slowdown, overproduction, or reduced consumption. Producer revenues shrink, and bankruptcies rise. | Opportunities in short-selling, inverse ETFs, or defensive assets. Focus shifts to risk management. |

| Trough | Prices stabilize at low levels. Underinvestment in production and recovering demand lay the foundation for the next upswing. Sentiment remains cautious. | Strategic entry point for long-term investors. Assets may be undervalued ahead of the next cycle. |

Timeframes of Commodity Cycles: From Months to Decades

These cycles occur across multiple time horizons, each with different drivers and implications:

- Short-term inventory cycles (months): Driven by seasonal demand, weather patterns, and supply chain dynamics. For example, natural gas prices often rise in winter due to heating demand.

- Medium-term business cycles (3-10 years): Tied to economic expansions and contractions. Capital spending, manufacturing output, and consumer spending influence demand for industrial metals and energy.

- Long-term supercycles (20-70 years): Also known as Kondratiev waves, these are driven by transformative shifts like urbanization, technological revolutions, or global industrialization. The current debate around a potential new supercycle centers on such structural changes.

What Drives Commodity Price Swings in the U.S. Market?

Commodity prices don’t shift randomly. They respond to powerful economic and geopolitical forces. Understanding these drivers helps investors anticipate turning points and adjust their strategies accordingly.

Supply and Demand: The Core Engine of Price Changes

At its foundation, commodity pricing hinges on global supply and demand. Disruptions-like a drought affecting soybean harvests or a mine closure reducing copper output-can send prices soaring. Conversely, technological breakthroughs such as fracking boosted U.S. shale oil production, flooding the market and driving oil prices lower in the mid-2010s. Inventory levels serve as a buffer, absorbing short-term shocks but offering early clues about future price direction.

Global and U.S. Economic Growth

Strong economic growth, especially in large economies like the U.S., China, and India, increases demand for raw materials. Industrial metals like copper and aluminum are barometers of infrastructure and manufacturing activity. Energy commodities such as crude oil and natural gas rise with transportation and production needs. During recessions, demand weakens, leading to price declines. U.S. GDP trends, industrial production data, and global manufacturing indexes are key indicators to monitor.

Inflation and Federal Reserve Policy

Commodities are widely seen as a hedge against inflation. When the dollar loses value, tangible assets like gold, oil, and agricultural goods often rise in price. The Federal Reserve’s monetary policy-particularly changes in interest rates and quantitative easing-plays a major role. Lower rates reduce the opportunity cost of holding non-yielding assets like commodities and can weaken the U.S. dollar, making dollar-denominated commodities cheaper for foreign buyers. Higher rates have the opposite effect. Investors track the Federal Open Market Committee (FOMC) meetings and inflation reports to gauge future price trends.

The Federal Reserve’s monetary policy decisions are closely watched for their ripple effects on commodity markets.

Geopolitical Risks and Supply Disruptions

Wars, sanctions, trade wars, and natural disasters can disrupt supply chains overnight. The Russia-Ukraine conflict in 2022, for instance, triggered sharp increases in wheat, nickel, and natural gas prices. The Middle East remains a flashpoint for oil supply concerns. Investors must account for geopolitical risk when evaluating long-term commodity exposure, particularly in energy and agriculture.

Technology and the Energy Transition

Innovation reshapes both supply and demand. Fracking revolutionized U.S. energy independence. Similarly, advances in battery technology and electric vehicles (EVs) are driving demand for lithium, cobalt, and rare earth elements. On the flip side, improved energy efficiency and solar adoption could reduce long-term fossil fuel demand. The pace of technological change can make some commodities obsolete while elevating others to strategic importance.

The U.S. Dollar’s Influence on Commodity Prices

Most major commodities are priced in U.S. dollars. When the dollar strengthens, it takes more foreign currency to buy the same amount of oil or gold, reducing demand and potentially lowering prices. A weaker dollar makes commodities cheaper for international buyers, increasing demand and supporting higher prices. Currency trends, therefore, are a critical factor in forecasting commodity performance.

Historical Commodity Cycles: What Past Trends Reveal for U.S. Investors

History offers valuable lessons about how commodity markets evolve and what patterns tend to repeat.

Post-WWII Reconstruction and Industrial Expansion

After World War II, global rebuilding efforts fueled a surge in demand for steel, copper, and energy. The U.S. emerged as an industrial powerhouse, and commodity prices rose steadily through the 1950s. This period exemplifies how post-crisis reconstruction can ignite a long-term commodity cycle.

The 1970s Oil Crises

Two major supply shocks-the 1973 Arab oil embargo and the 1979 Iranian Revolution-halved oil production in key regions, sending prices skyrocketing. U.S. gasoline prices spiked, inflation soared, and the economy entered a period of stagflation. These events highlighted the vulnerability of modern economies to energy supply disruptions and cemented oil’s role as a geopolitical lever.

The 2000s Commodity Boom

One of the most significant commodity supercycles in modern history unfolded between 2000 and 2008, driven by China’s rapid industrialization. Chinese demand for iron ore, copper, and oil surged, pushing prices to record highs. Oil hit $147 per barrel in 2008, while gold and base metals saw multi-year rallies. The boom ended abruptly with the global financial crisis, which crushed demand and triggered a sharp correction.

The 2015 Commodity Crisis

After a partial recovery, commodity markets crashed in 2015. Prices for oil, copper, and iron ore plummeted due to slowing Chinese growth, a strong U.S. dollar, and oversupply from U.S. shale producers. Oil dropped from over $100 to below $30 per barrel, wiping out billions in market value. This downturn underscored the risks of overreliance on emerging market demand and the impact of supply-side innovation.

Recent Volatility: 2021-2023 Market Shifts

The pandemic recovery sparked a new wave of price increases. Stimulus spending, supply chain bottlenecks, and low interest rates drove demand for everything from lumber to semiconductors. The 2022 invasion of Ukraine intensified the rally, particularly in energy and agriculture. Prices for natural gas, wheat, and nickel spiked, demonstrating how fast-moving events can disrupt markets.

The World Bank provides regular analysis of commodity market trends, offering historical data and forward-looking forecasts.

Is a New Commodity Supercycle Emerging in 2025?

Many analysts are debating whether the world is entering a new commodity supercycle, one driven not by industrialization but by decarbonization and supply constraints.

Case for a New Supercycle

Several long-term trends support the idea of a sustained upswing:

- Green Energy Transition: The shift to EVs, wind, and solar requires massive amounts of copper, lithium, and nickel. The U.S. Inflation Reduction Act and similar global policies are accelerating demand.

- Infrastructure Investment: The Bipartisan Infrastructure Law is funneling $1.2 trillion into U.S. roads, bridges, and power grids-boosting demand for steel, aluminum, and construction materials.

- Reshoring and Supply Chain Resilience: Companies are relocating production to North America, increasing domestic demand for raw inputs and reducing reliance on foreign supply chains.

- Underinvestment in Supply: Years of low returns and ESG pressures have led to underfunding in oil, gas, and mining projects. This could result in supply shortages as demand rebounds.

- Inflation and Dollar Dynamics: Persistent inflation and potential shifts in Fed policy could keep real interest rates low, supporting commodity prices.

Arguments Against a Sustained Supercycle

Skeptics caution that past cycles have been overestimated. Key counterpoints include:

- Technological Substitution: Advances in recycling, battery chemistry, and material efficiency could reduce the need for new mining.

- Demand Destruction: High prices may force industries to innovate or switch to alternatives, as seen with natural gas during price spikes.

- Global Economic Slowdown: Rising interest rates and debt levels may dampen growth, limiting commodity demand.

- Policy Uncertainty: The pace of green investment depends on government funding, permitting, and political stability.

Expert Outlooks and U.S. Market Implications

Analysts are divided. Some banks project strong demand for copper and lithium through 2030, while others warn of cyclical peaks and potential overcapacity. For U.S. investors, the key is to differentiate between structural growth (e.g., EV adoption) and temporary spikes (e.g., post-pandemic inventory rebuilding).

If a supercycle takes hold, sectors like mining, renewable energy, and infrastructure could thrive. However, higher input costs may pressure manufacturers and consumers, contributing to inflation and potentially slowing economic growth.

Investment Strategies for Navigating Commodity Cycles in 2025

Successfully navigating commodity market cycles requires a mix of strategic positioning, risk control, and access to the right tools.

Strategic Asset Allocation: Adding Commodities to Your Portfolio

Commodities typically have low correlation with stocks and bonds, making them a valuable diversification tool. Allocating 5%-10% of a portfolio to commodities can improve risk-adjusted returns, especially during inflationary periods. The optimal allocation depends on risk tolerance, time horizon, and macroeconomic outlook.

Direct Investment Options: Futures, Options, and ETFs

U.S. investors have several ways to gain direct exposure:

- Futures contracts: Standardized agreements to buy or sell a commodity at a set price and date. Traded on U.S. exchanges like the CME Group, they offer leverage but require careful risk management.

- Options: Provide flexibility to hedge or speculate with limited downside. Useful for managing volatility without full exposure.

- Commodity ETFs: Offer accessible, liquid exposure. Examples include USO (crude oil), GLD (gold), and DBA (agricultural commodities). Some ETFs track futures, others hold physical assets.

Indirect Investment: Equities of Commodity Producers

Investing in stocks of companies tied to commodities provides exposure with added benefits like dividends and company-specific growth. Examples include:

- Mining firms: Freeport-McMoRan (copper), Newmont (gold)

- Energy producers: ExxonMobil, Chevron

- Agricultural and equipment firms: Archer-Daniels-Midland, Deere & Company

These stocks often outperform during bull markets but can be more volatile than direct commodity exposure.

Hedging Against Inflation and Price Swings

For investors concerned about inflation or cost volatility, commodities serve as a natural hedge. Gold has long been a store of value during uncertainty. Energy and agricultural commodities can protect against rising living costs. Businesses can use futures to lock in input prices, while investors can use ETFs or options to limit downside.

Managing Risk in Volatile Markets

Commodity trading involves high volatility and leverage. Futures positions can generate large gains-or losses-quickly. To manage risk:

- Use stop-loss orders to limit downside.

- Avoid over-leveraging, especially in fast-moving markets.

- Monitor market sentiment, inventory reports (e.g., EIA crude oil data), and macroeconomic indicators.

- Stay informed about geopolitical developments and supply chain updates.

Top Brokers for Trading Commodity Cycles in the U.S. (2025)

Choosing the right broker is critical for accessing commodity markets efficiently and securely.

Why Regulation Matters for U.S. Commodity Traders

U.S. investors should only trade with brokers regulated by the Commodity Futures Trading Commission (CFTC) and the National Futures Association (NFA). These agencies enforce capital requirements, transparency rules, and customer protection standards. For international brokers serving global clients, holding an FCA license (like Moneta Markets) adds an extra layer of credibility and oversight.

Key Factors in Broker Selection

When evaluating platforms, consider:

- Instrument availability: Does the broker offer futures, ETFs, CFDs, or options on your target commodities?

- Trading platforms: Are they reliable, intuitive, and equipped with charting and analysis tools?

- Fees and spreads: Low trading costs can significantly improve net returns, especially for active traders.

- Customer service: Responsive support is crucial during fast-moving markets.

- Educational resources: Tutorials, webinars, and market analysis help investors build expertise.

Broker Comparison: Leading Platforms for U.S. Commodity Access

| Broker | Key Advantages for Commodity Trading | U.S. Regulation | Platform Features |

|---|---|---|---|

| Moneta Markets | Offers highly competitive spreads across energy, metals, and agricultural commodities. Features robust MT4 and MT5 platforms, extensive educational content, dedicated client support, and global regulatory oversight, including an FCA license. Ideal for U.S. traders seeking diverse CFDs and advanced tools to navigate market cycles. | Regulated globally with FCA oversight; U.S. clients may access services through international entities where permitted. | MT4, MT5, WebTrader. Advanced charting, algorithmic trading, expert advisors. |

| FOREX.com | A major U.S.-regulated platform with strong commodity CFD and futures access. Offers competitive pricing and a range of research tools tailored to active traders. | CFTC, NFA | MetaTrader 4, MetaTrader 5, Proprietary Web Trading, Desktop. |

| IG | Global leader with access to over 17,000 markets, including extensive commodity CFDs and futures. Known for advanced charting (ProRealTime) and in-depth market analysis. | CFTC, NFA | Proprietary Web Platform, Mobile App, MT4. |

| OANDA | Trusted for user-friendly interfaces and transparent pricing. Offers a solid selection of forex and CFD instruments, with strong CFTC/NFA compliance. | CFTC, NFA | fxTrade (proprietary), MetaTrader 4, Web. |

Note: Product availability, including CFDs, may vary for U.S. residents due to regulatory restrictions. Always confirm offerings with the broker directly.

Conclusion: Mastering Commodity Cycles in a Changing U.S. Economy

Commodity market cycles are a defining feature of the global financial system-and a powerful force shaping the U.S. economy. Whether driven by short-term inventory swings or decades-long structural shifts, these cycles create both risk and opportunity. As 2025 unfolds, investors face a complex landscape shaped by inflation, energy transition, and geopolitical uncertainty. Success will depend on understanding the phases of the cycle, recognizing key drivers, and applying disciplined strategies. Diversification, hedging, and access to reliable trading platforms are essential tools. Brokers like Moneta Markets, with competitive pricing, advanced platforms, and FCA-regulated operations, can empower traders to act decisively. Staying informed, adaptable, and strategically positioned will be the hallmark of those who thrive in the next chapter of commodity market evolution.

What are the main phases of commodity market cycles?

The main phases of commodity market cycles are Expansion (prices rising), Peak (prices at their highest), Contraction (prices falling), and Trough (prices at their lowest). Understanding these phases helps investors anticipate market movements.

How do commodity market cycles affect the US economy?

Commodity market cycles significantly affect the US economy by influencing inflation rates, corporate profits of commodity-producing companies, consumer spending power, and the overall balance of trade. For example, rising energy prices can lead to higher gas prices and increased manufacturing costs, impacting consumers and businesses alike.

Is there a “Commodity Supercycle” currently impacting the United States?

There is ongoing debate among experts regarding whether a new “Commodity Supercycle” is emerging, particularly driven by the green energy transition, global infrastructure spending, and potential deglobalization trends. While some indicators point to long-term upward pressure on certain commodities, others caution against sustained, broad-based price increases. US investors should monitor these discussions closely for 2025.

Where can I find a reliable “Commodity Market Cycles Chart” or graph for historical data?

Reliable “Commodity Market Cycles Chart” or graphs for historical data can be found from reputable financial news outlets (e.g., Bloomberg, Wall Street Journal), economic research institutions like the World Bank, or directly from data providers like the Federal Reserve Economic Data (FRED). Many online trading platforms also offer historical charting tools.

How can US investors prepare for potential commodity crises in 2025?

US investors can prepare for potential commodity crisis 2025 by diversifying their portfolios, maintaining adequate cash reserves, and utilizing hedging strategies. Understanding the drivers of commodity downturns, such as slowing global growth or oversupply, can help investors adjust their positions proactively. Brokers like Moneta Markets offer various instruments and educational resources that can aid in risk management during volatile periods.

What role does inflation play in commodity market cycles in the US?

Inflation plays a significant role in commodity market cycles in the US. Commodities are often seen as a hedge against inflation because their prices tend to rise when the purchasing power of the US Dollar declines. During periods of high inflation, investors often flock to commodities, driving prices higher and potentially extending the expansion phase of a cycle.

Which commodities are most influenced by market cycles for US traders?

For US traders, energy commodities (crude oil, natural gas), precious metals (gold, silver), industrial metals (copper, aluminum), and agricultural commodities (corn, wheat, soybeans) are most heavily influenced by market cycles. Their prices are highly sensitive to global economic growth, supply disruptions, and geopolitical events.

What are the best strategies for investing in commodity cycles in the United States in 2025?

For investing in commodity cycles in the United States in 2025, effective strategies include strategic asset allocation, direct investments via futures, options, or ETFs, and indirect investments in stocks of commodity-producing companies. Utilizing a broker like Moneta Markets can facilitate access to a wide range of commodity CFDs with competitive spreads and advanced trading platforms, making it easier to implement these strategies and capitalize on market movements.

Be First to Comment